Understanding Capital Gains Tax on Commercial Real Estate Sales

When you sell a commercial property for a profit, the IRS wants its share. However, unlike selling a stock, calculating the tax bill for real estate is a multi-layered process. It’s not simply a matter of paying a flat percentage on your profit; the “how” and “how long” of your ownership matter immensely.

- Short-term vs. long-term gains matter

- Depreciation recapture increases your tax liability

- High-income surtax (NIIT) may apply

- 1031 Exchange preserves equity

- Effective tax rate can consume a significant portion of profits

Investors Keep When Selling Commercial Property

Capital Gains Timing

The duration of ownership directly affects your tax rate:

Short-term gains (sold within 1 year) are taxed as ordinary income, potentially up to 37%.

Long-term gains (held over 1 year) enjoy lower rates—typically 15%–20%. Timing your sale can maximize after-tax proceeds.

Depreciation Recapture

This is where commercial real estate investors often get blindsided. Over the years, you likely claimed depreciation deductions to lower your annual tax bill. When you sell, the IRS “recaptures” that benefit. The portion of your gain attributed to those depreciation deductions is not taxed at the 20% capital gains rate; it is taxed at a special Unrecaptured Section 1250 gain rate of 25%.

Net Investment Income Tax (NIIT)

High-income earners generally face an additional hurdle. If your Modified Adjusted Gross Income (MAGI) exceeds $200,000 (single) or $250,000 (married filing jointly), you will likely owe an extra 3.8% Net Investment Income Tax on your capital gains.

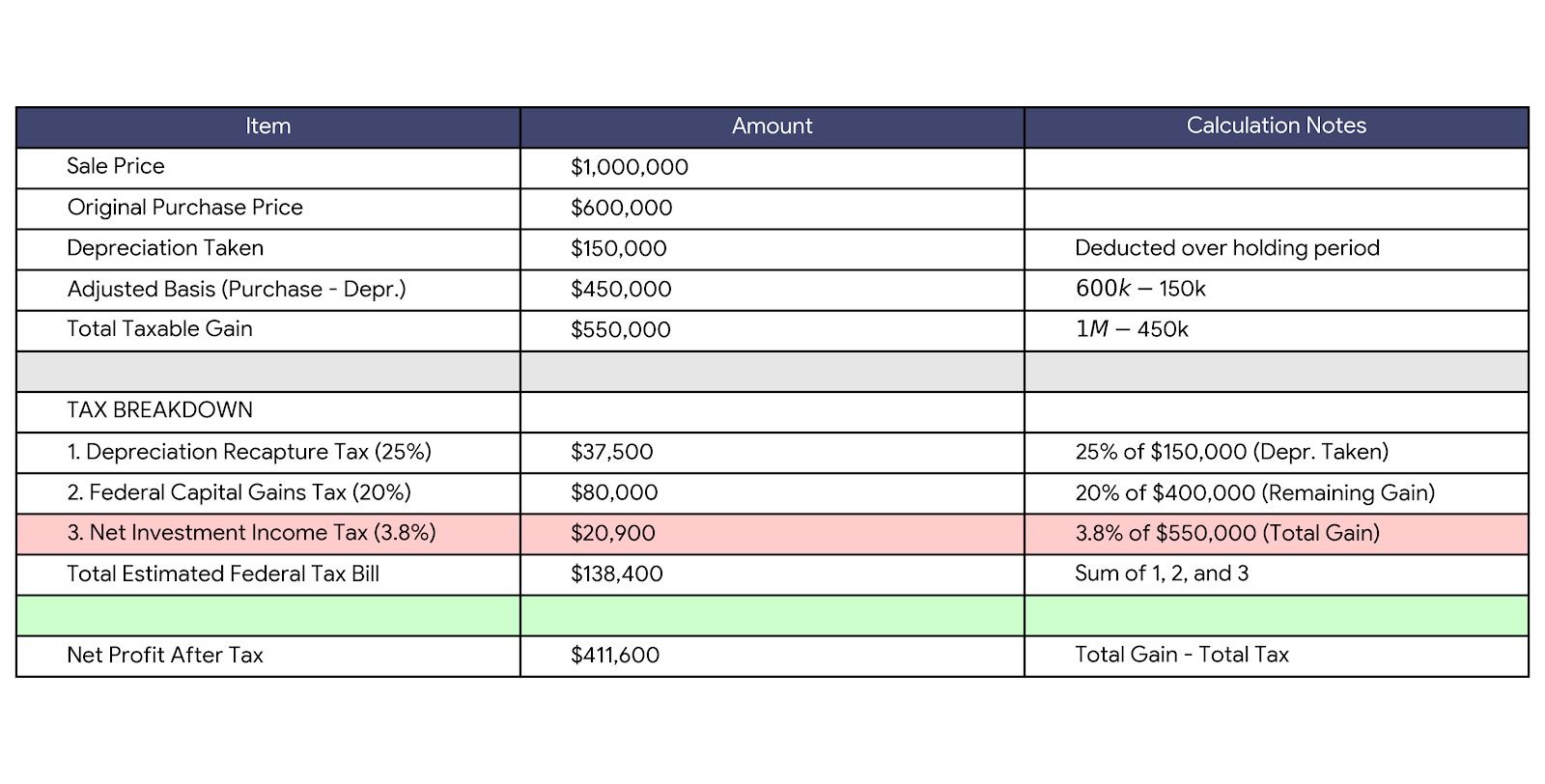

Hypothetical Tax Breakdown: $1M Commercial Property Sale

Hypothetical Scenario:

Sale Price: $1,000,000

Original Purchase Price: $600,000

Depreciation Claimed: $150,000

Tax Bite Calculator

| Item | Amount | Calculation Notes |

|---|---|---|

| Sale Price | $1,000,000 | |

| Original Purchase Price | $600,000 | |

| Depreciation Taken | $150,000 | Deducted over holding period |

| Adjusted Basis | $450,000 | Purchase Price – Depreciation |

| Total Taxable Gain | $550,000 | Sale Price – Adjusted Basis |

TAX BREAKDOWN

| Item | Amount | Notes |

|---|---|---|

| Depreciation Recapture Tax (25%) | $37,500 | 25% of $150,000 |

| Federal Capital Gains Tax (20%) | $80,000 | 20% of $400,000 |

| Net Investment Income Tax (3.8%) | $20,900 | 3.8% of $550,000 |

| Total Estimated Federal Tax Bill | $138,400 | Sum of 1, 2, and 3 |

| Net Profit After Tax | $411,600 | Total Gain – Total Tax |

Maximizing Net Proceeds When Selling Commercial Property

Many property owners focus only on market timing, but savvy investors also consider tax implications, depreciation recapture, and reinvestment opportunities. Planning ahead ensures you retain the maximum value from a sale.

- Plan Around Capital Gains Timing – Selling at the right time can significantly reduce tax liability.

- Manage Depreciation Recapture Risk – Knowing this in advance allows for strategic sale structuring.

- Leverage 1031 Exchange for Strategic Reinvestment – Roll sale proceeds into new properties to defer taxes entirely.

Conclusion

For a high-earner selling a long-held building, the effective federal tax rate often blends the 20% capital gains rate, the 25% recapture rate, and the 3.8% NIIT. Because this can amount to a significant chunk of your equity, many investors utilize a 1031 Exchange to defer these taxes entirely and roll the full proceeds into a new asset.

Understanding Capital Gains Tax on Commercial Real Estate Sales

When you sell a commercial property for a profit, the IRS wants its share. However, unlike selling a stock, calculating the tax bill for real estate is a multi-layered process. It’s not simply a matter of paying a flat percentage on your profit; the “how” and “how long” of your ownership matter immensely.

- Short-term vs. long-term gains matter

- Depreciation recapture increases your tax liability

- High-income surtax (NIIT) may apply

- 1031 Exchange preserves equity

- Effective tax rate can consume a significant portion of profits

Investors Keep When Selling Commercial Property

Capital Gains Timing

The duration of ownership directly affects your tax rate:

Short-term gains (sold within 1 year) are taxed as ordinary income, potentially up to 37%.

Long-term gains (held over 1 year) enjoy lower rates—typically 15%–20%. Timing your sale can maximize after-tax proceeds.

Depreciation Recapture

This is where commercial real estate investors often get blindsided. Over the years, you likely claimed depreciation deductions to lower your annual tax bill. When you sell, the IRS “recaptures” that benefit. The portion of your gain attributed to those depreciation deductions is not taxed at the 20% capital gains rate; it is taxed at a special Unrecaptured Section 1250 gain rate of 25%.

Net Investment Income Tax (NIIT)

High-income earners generally face an additional hurdle. If your Modified Adjusted Gross Income (MAGI) exceeds $200,000 (single) or $250,000 (married filing jointly), you will likely owe an extra 3.8% Net Investment Income Tax on your capital gains.

04. Hypothetical Tax Breakdown: $1M Commercial Property Sale

Hypothetical Scenario:

Sale Price: $1,000,000

Original Purchase Price: $600,000

Depreciation Claimed: $150,000

Tax Bite Calculator

| Item | Amount | Calculation Notes |

|---|---|---|

| Sale Price | $1,000,000 | |

| Original Purchase Price | $600,000 | |

| Depreciation Taken | $150,000 | Deducted over holding period |

| Adjusted Basis | $450,000 | Purchase Price – Depreciation |

| Total Taxable Gain | $550,000 | Sale Price – Adjusted Basis |

TAX BREAKDOWN

| Item | Amount | Notes |

|---|---|---|

| Depreciation Recapture Tax (25%) | $37,500 | 25% of $150,000 |

| Federal Capital Gains Tax (20%) | $80,000 | 20% of $400,000 |

| Net Investment Income Tax (3.8%) | $20,900 | 3.8% of $550,000 |

| Total Estimated Federal Tax Bill | $138,400 | Sum of 1, 2, and 3 |

| Net Profit After Tax | $411,600 | Total Gain – Total Tax |

Maximizing Net Proceeds When Selling Commercial Property

Many property owners focus only on market timing, but savvy investors also consider tax implications, depreciation recapture, and reinvestment opportunities. Planning ahead ensures you retain the maximum value from a sale.

- Plan Around Capital Gains Timing – Selling at the right time can significantly reduce tax liability.

- Manage Depreciation Recapture Risk – Knowing this in advance allows for strategic sale structuring.

- Leverage 1031 Exchange for Strategic Reinvestment – Roll sale proceeds into new properties to defer taxes entirely.

Conclusion

For a high-earner selling a long-held building, the effective federal tax rate often blends the 20% capital gains rate, the 25% recapture rate, and the 3.8% NIIT. Because this can amount to a significant chunk of your equity, many investors utilize a 1031 Exchange to defer these taxes entirely and roll the full proceeds into a new asset.